The Power of Compounding

Compounding is when your money starts earning returns on the returns it already made — like a snowball growing bigger as it rolls downhill.

Example:

If you invest ₹10,000 at 10% annual return:

- After 1 year → ₹11,000

- After 10 years → ₹25,937

- After 20 years → ₹67,275

You didn’t just double your money — you made it grow 6.7 times, without doing anything extra.

That’s the magic of time + patience = wealth.

Why You Should Invest?

Let’s start with a simple question: Why do people invest at all?

If you ask around, you’ll hear a dozen different answers —

“To get rich.”

“To beat inflation.”

“To save for retirement.”

“Because my friend told me to.” 😄

All of these are partly true, but the real reason is deeper:

We invest because we want control over our future — not uncertainty.

Let’s break this down and make it crystal clear with examples you’ll feel, not just read.

1. Saving Alone Isn’t Enough

Most of us grew up hearing this advice:

“Save money, and you’ll be safe.”

That was fine once upon a time.

But today, saving isn’t enough to grow your wealth — it only helps you “store” it.

Why? Because of one silent enemy: inflation.

Inflation: The Invisible Thief

Inflation is the gradual rise in prices of goods and services — meaning, your ₹100 today won’t buy the same things 10 years from now.

Let’s look at an example to understand this scenario:

- In 2010, 1 litre of milk cost ₹25.

- In 2025, the same litre costs ₹60.

That’s more than double!

If you had ₹1 lakh saved in 2010, and kept it idle in your savings account (earning around 3% interest),

your “real value” today is much less — because prices around you went up faster than your money grew.

So even though your balance increased, your buying power decreased.

That’s the real danger of not investing.

3. Your Goals Need Money, Not Just Hope

Everyone has goals — big or small:

- Buying your first home

- Sending kids to college

- Retiring comfortably

- Travelling the world

But goals are just dreams unless you give them a financial shape.

Here’s where investing bridges the gap between “someday” and “sooner”.

To make this clearer, let’s take an example.:

Let’s say you want ₹25 lakh for your child’s higher education in 15 years.

If you keep money in a savings account (3% return):

→ You’ll need to save about ₹11,800 every month.

But if you invest smartly (assuming 12% return):

→ You’ll only need to invest ₹6,200 per month.

That’s half the effort for the same result — all because you made your money work harder.

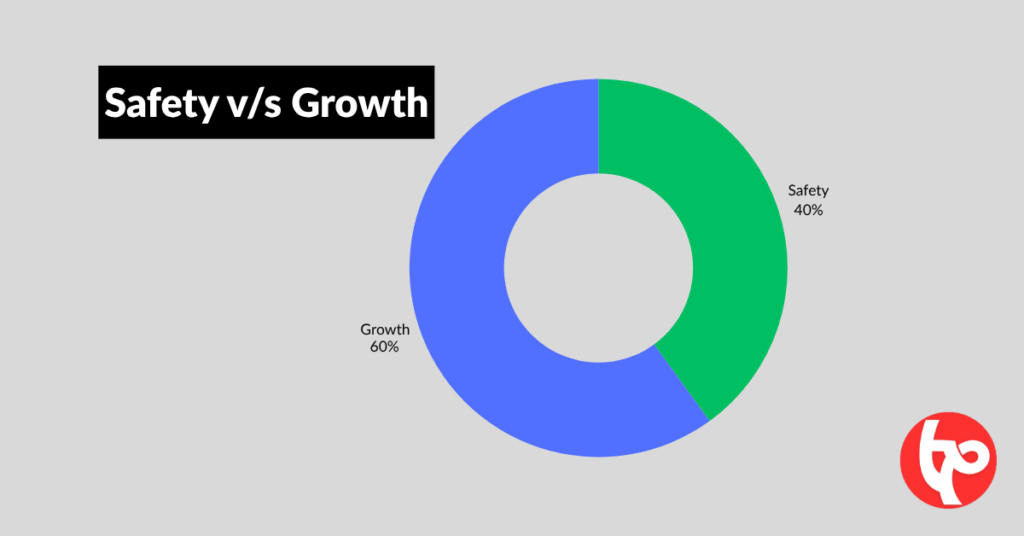

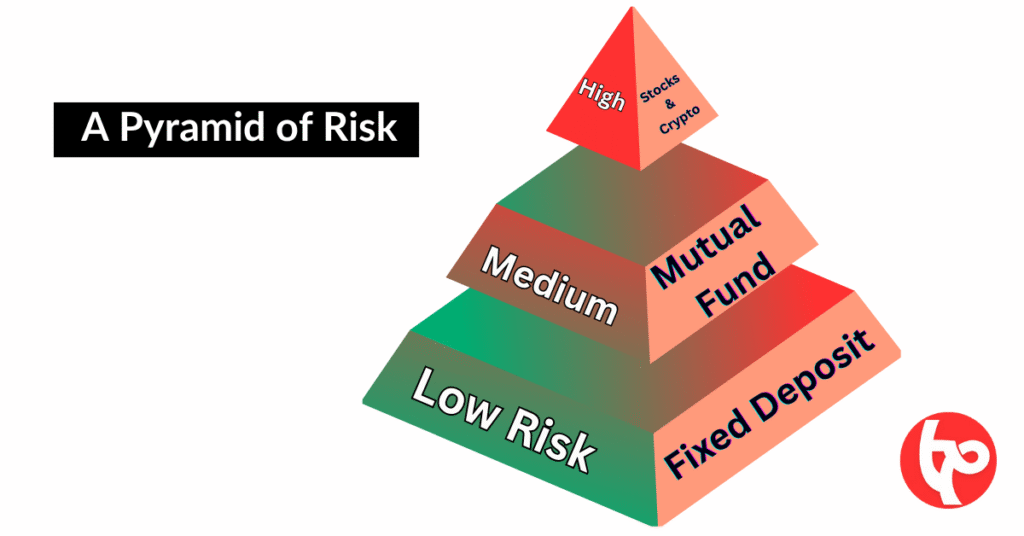

4. Investing Balances Risk and Reward

There’s a misconception that investing means taking big risks.

In reality, you can choose your own comfort zone — from super-safe to aggressive.

Let’s compare:

Type | Example | Risk | Average Return | Suitable For |

Safe | Bank FD, PPF | Low | 6–8% | Stability seekers |

Moderate | Mutual Funds, Index Funds | Medium | 10–14% | Balanced investors |

Aggressive | Stocks, Equity Funds | High | 12–20% | Long-term growth seekers |

When you understand how each investment works, you can build a mix —

some safe, some growth-oriented — so your money grows without sleepless nights.

Example:

If you invest ₹10,000 a month —

- ₹4,000 in safe assets (PPF, FD)

- ₹6,000 in growth assets (mutual funds, stocks)

→ you reduce overall risk while still compounding wealth.

That’s called diversification, and it’s your best friend in uncertain markets.

5. Financial Independence Means Freedom

At the heart of investing lies one simple goal — freedom.

Freedom to:

- Quit a job you dislike

- Take a break without guilt

- Help your parents without stress

- Start something of your own

- Sleep peacefully knowing your future is secure

Example:

Meet Neha, a teacher who started investing ₹8,000/month in mutual funds at 27.

Now, at 40, her portfolio is worth ₹32 lakh.

She says,

“I don’t worry about retirement anymore — I’m planning my travel bucket list instead.”

That’s what real financial independence looks like — peace of mind, not just numbers in a bank.

6.Because the Earlier You Learn, the Better You Play

Let’s face it — schools taught us algebra and trigonometry, but not money management.

We learned how to earn, but not how to grow or protect it.

The good news?

It’s never too late to start — but the earlier you do, the easier life becomes later.

Example:

Think of investing like planting a mango tree.

The best time was 10 years ago.

The second-best time? Today.

If you plant the seed today, you might wait a few years for fruit —

but once it grows, it’ll feed you for decades.

That’s the magic of consistency in investing.

7. Wealth Creation Is a Journey, Not a Race

Everyone’s path looks different.

Some start at 22, some at 40.

Some invest ₹2,000 a month, others ₹20,000.

And that’s okay.

The key is not how fast you go, but how long you stay.

If you drive steadily for 20 years, you’ll reach further than someone who speeds for 2 and quits after a crash.

Markets work the same way — discipline beats excitement.

In Short

You should invest because:

- Inflation silently eats your savings.

- Compounding multiplies your patience.

- Your dreams need funding, not wishing.

- Risk is manageable with smart planning.

- Freedom is built through consistency.

Final Thought Before We Move On

“You can make money only two ways —

work for it, or make it work for you.”

When you start investing, you give every rupee a job.

And over time, those rupees bring friends back with interest 😄.

Bank Fixed Deposits (FDs) — The Safe Starter

This is where most Indians begin.

FDs are like your safety blanket — they give you peace of mind, but not much excitement.

How it works:

You deposit a fixed amount of money for a fixed period (say 1–5 years), and the bank pays you a fixed interest (usually 6–7% per annum).

Example:

You invest ₹1 lakh for 3 years at 7% interest.

At the end, you’ll get around ₹1.23 lakh — no surprises, no risks.

Pros:

- 100% predictable and safe

- Easy to start from your bank account

- Suitable for short-term goals

Cons:

- Returns often lower than inflation

- Tax on interest income

- Money locked-in till maturity

When to invest:

If you’re new to investing or saving for short-term needs (like a trip or emergency fund), FDs are a good start.

Shares & Stocks

The stock market is a platform where companies raise money and investors participate in ownership. To understand how indexes, returns, and benchmarks work, you can refer to the National Stock Exchange (NSE) official Nifty 50 index methodology.

When you buy a stock, you literally own a part of that company.

If the company grows, your money grows too.

Think of it like this:

Buying one share of Infosys makes you a tiny shareholder of Infosys itself — a part-owner of a billion-dollar enterprise.

Example:

If you bought 100 shares of Infosys at ₹1,000 each in 2013 (₹1 lakh total), by 2025, your investment would be worth around ₹2.8 lakh — almost 3x your money, not including dividends.

Pros:

- High potential returns

- Dividends + capital appreciation

- Liquidity — you can buy/sell anytime

Cons:

- Volatile in the short term

- Requires research and patience

- Emotional decisions can hurt returns

When to invest:

If you can stay invested for 5+ years and can handle ups and downs, stocks are your long-term wealth creators.

Mini Tip:

Start small — pick companies you understand.

If you use Zomato daily, try reading about its financials and story. Investing becomes easier when you relate to the business.

Gold — The Time-Tested Safe Haven

Indians love gold — and not just for weddings!

It’s been a symbol of security and wealth preservation for centuries.

But you don’t need to buy jewelry to invest in gold anymore — there are smarter options like Gold ETFs and digital gold.

Example:

From 2013 to 2023, gold prices rose from ₹27,000 to ₹60,000 per 10 grams — a CAGR of around 8%.

Not spectacular, but solid protection during market crashes.

Pros:

- Hedge against inflation and currency risk

- Easy to buy/sell

- Works well in economic uncertainty

Cons:

- No regular income

- Returns lower than equities over time

When to invest:

Use gold as a stabilizer — 5–10% of your portfolio to balance market risk.

Real Estate

Owning property is the dream of many — a home you can see, touch, and live in.

Real estate can be both a consumption asset (your home) and an investment asset (a rented or resold property).

Example:

A flat bought for ₹40 lakh in 2010 could be worth ₹1.2 crore today — roughly 7–8% annual appreciation, plus rent income.

Pros:

- Tangible and stable

- Potential rental income

- Hedge against inflation

Cons:

- Requires large capital

- Low liquidity

- Maintenance and legal risks

When to invest:

For long-term wealth preservation, or if you seek rental income.

But don’t lock all your money here — balance with liquid investments.

New-Age Investments — Crypto, REITs, ETFs, and Beyond

Welcome to the modern investing playground .

Here you’ll find digital assets, fractional real estate, and innovative products built for tech-savvy investors.

🔹 Crypto (Bitcoin, Ethereum, etc.)

Digital currencies based on blockchain.

High reward but very high risk.

Example:

Bitcoin went from ₹30,000 in 2013 to over ₹50 lakh in 2025 — but also dropped 70% multiple times in between.

🔹 REITs (Real Estate Investment Trusts)

You invest in property portfolios — malls, offices, etc. — and earn rental income as dividends.

A great way to get real estate exposure without buying property.

🔹 ETFs (Exchange Traded Funds)

These track indexes like the Sensex or Nifty 50 — giving you broad market exposure at low cost.

Pros (for new-age options):

- Innovative and flexible

- Lower entry barriers

- Great for diversification

Cons:

- Market-linked risk

- Requires awareness and caution

Comparing All Investment Types

Investment Type | Risk | Return (p.a.) | Liquidity | Suitable For |

Bank FD | Low | 6–7% | High | Short-term stability |

Mutual Funds | Medium | 10–14% | High | Long-term goals |

Stocks | High | 12–20% | Very High | Growth seekers |

Bonds | Low-Medium | 7–9% | Medium | Regular income |

Gold | Low-Medium | 7–8% | High | Safety & diversification |

Real Estate | Medium | 7–10% | Low | Wealth building |

Crypto / New-age | Very High | Variable | High | Risk-takers |

Final Thought Before Moving On

“There’s no single ‘best investment.’

The best one is the one that fits your goal, your timeline, and your comfort.”

In the next section, we’ll discuss how to actually build your first investment plan — setting goals, choosing asset mix, and starting small but smart.

Analyze Your Current Financial Situation

Before deciding how much to invest, take stock of your current finances — just like a doctor runs diagnostics before prescribing medicine.

You need to know:

- How much you earn monthly

- How much you spend

- How much you save

- How much debt you have

Suppose your monthly income is ₹60,000.

You spend ₹40,000 on essentials and ₹5,000 on discretionary items.

That leaves ₹15,000 in savings potential — your investable surplus.

But if you have an EMI of ₹8,000, you should ideally invest ₹6,000 and keep ₹1,000 aside for emergencies.

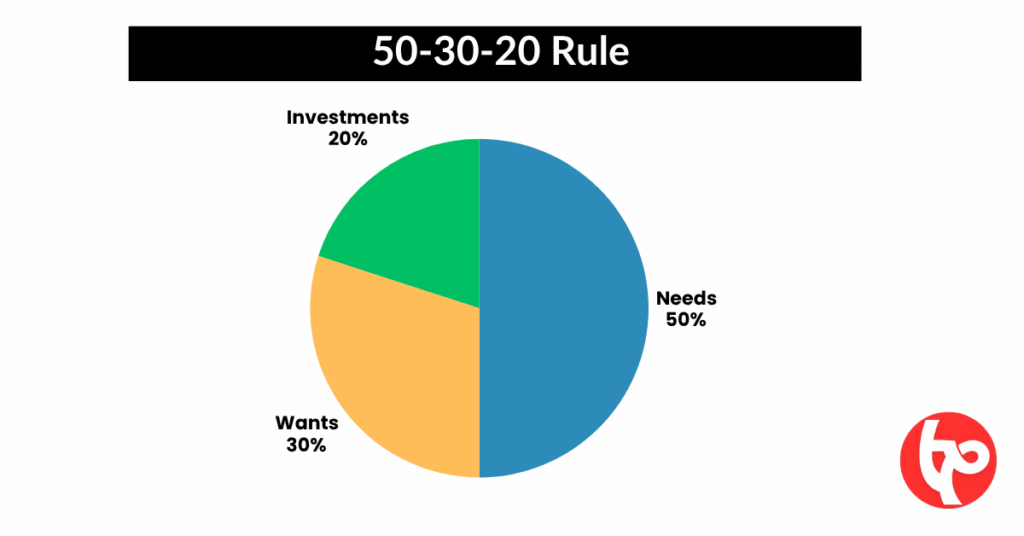

Use the 50-30-20 rule:

- 50% for needs

- 30% for wants

- 20% for savings/investments

This simple rule keeps your finances balanced while ensuring consistent investing.

Decide Your Risk Appetite

Everyone talks about returns, but real investors first understand risk.

Risk appetite means — how much fluctuation in value can you handle without losing sleep at night?

Let’s break this down with an example

Rina vs. Karan

- Rina (28): Just started working, no major responsibilities.

She can take high risk → invests mostly in equity mutual funds. - Karan (40): Has a family, home loan, and school expenses.

He prefers low-risk → more focus on debt funds and gold.

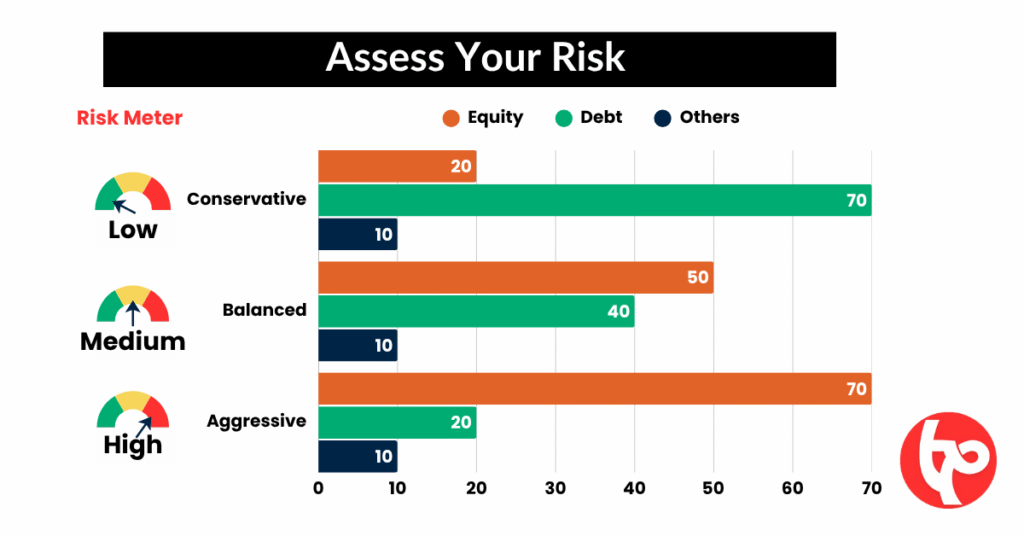

How to Assess Your Risk Appetite

Profile | Description | Suggested Allocation (Equity : Debt : Others) |

Conservative | Prioritizes safety, dislikes volatility | 20 : 70 : 10 |

Balanced | Open to moderate ups and downs | 50 : 40 : 10 |

Aggressive | Comfortable with market swings for higher returns | 70 : 20 : 10 |

Allocate Assets Smartly

Asset allocation is the backbone of investing.

It means deciding how much money to put into different investment types — like stocks, bonds, gold, etc.

A great investor once said:

“Don’t put all your eggs in one basket — but don’t scatter them in every field either.”

A simple thumb rule: 100 – Your Age = % of Portfolio in Equities

So if you’re 30, you could keep ~70% in equities (stocks/mutual funds) and 30% in debt (FDs, bonds, etc.).

As you age, gradually reduce risk.

Remember Meena (from our earlier story)? She is 25.

She invests ₹5,000 monthly:

- ₹3,500 in mutual funds (equity)

- ₹1,000 in debt fund

- ₹500 in gold ETF

That’s 70-20-10 — a simple, balanced mix for her age and goals.

Start Small but Stay Consistent

Many people wait until they “have enough money” to start investing.

But waiting is the biggest cost.

Start with what you can — even ₹500 a month matters.

It’s not about the amount; it’s about consistency and compounding.

A ₹1,000 SIP growing at 12% per year becomes:

- ₹2 lakh in 10 years

- ₹10 lakh in 25 years

That’s the power of staying invested.

Useful Tip:

Automate your SIPs on salary day. Treat investing as a non-negotiable bill to your future self.

Avoid Common Mistakes

New investors often trip on the same stones.

Mistake | Why It’s Dangerous | Fix |

Chasing “hot tips” | Emotion > logic = loss | Invest based on research, not rumors |

Timing the market | Impossible consistently | Time in the market beats timing |

Ignoring diversification | Concentrated risk | Mix assets wisely |

Withdrawing early | Miss compounding | Stay patient |

No emergency fund | Forced selling during need | Keep 3–6 months’ expenses in liquid fund |

Create Your First Investment Plan Template

Here’s a simple structure you can actually use:

Goal | Time Frame | Monthly Investment | Investment Type | Expected Return | Notes |

Emergency Fund | 1 year | ₹5,000 | Liquid Fund | 6% | 3–6 months’ expenses |

Europe Trip | 4 years | ₹8,000 | Hybrid MF | 9% | Medium risk |

Retirement | 30 years | ₹10,000 | Equity MF | 12% | Start SIP |

Key Takeaway

“An investment plan isn’t a one-time document — it’s a living roadmap.

Review it every year, adjust as your life changes, and stay focused on the big picture.”

This is where most people stop — but real investors go one step further.

They learn to measure performance, rebalance portfolios, and upgrade their knowledge consistently.

That’s exactly what we’ll cover next:

How to Track, Review, and Improve Your Investments Over Time

If you’ve made it this far, you’ve already done something 90% of people never do — you’ve started your investment journey.

But here’s the truth most beginners miss:

Investing isn’t a one-time event — it’s a lifelong relationship with your money.

You don’t just “set it and forget it.”

You nurture it, check its progress, fix it when it goes off track, and grow smarter every year.

Let me tell you a short story to make this real.

Riya vs. Aman — The Tale of Two Investors

Riya and Aman both began investing ₹10,000 every month in mutual funds.

- Riya treated investing like a chore she could tick off once. She set up her SIPs and never looked back.

- Aman, on the other hand, made it a habit to review his portfolio every 6 months.

After 5 years, here’s what happened:

- Riya’s SIPs were still running — but half of them had underperformed because the fund manager’s strategy changed.

- Aman’s portfolio, meanwhile, grew 25% more. Why? Because he switched poor performers, rebalanced his mix, and even increased his SIPs when his salary grew.

Tracking and reviewing doesn’t just protect your money — it multiplies it.

Why Tracking Matters

Imagine driving a car without a dashboard.

You wouldn’t know your speed, fuel level, or direction — until something goes wrong.

That’s exactly what happens when you invest and never track.

Tracking your investments helps you:

- Know if you’re on track to meet your goals.

- See what’s performing and what’s not.

- Identify when to adjust your plan — before small issues become big problems.

And guess what? You don’t need to be a finance geek to do it.

You just need a simple system.

How to Track Your Investments

Let’s break this into two easy ways:

Option 1: Manual Tracking (Google Sheets)

Option 1: Manual Tracking (Google Sheets)

If you like doing things your way, create a sheet with:

Date | Investment Type | Amount | Current Value | Returns (%) | Notes |

Jan 2024 | SIP (Axis Bluechip Fund) | ₹10,000 | ₹12,000 | 20% | Continue |

Jan 2024 | Gold ETF | ₹5,000 | ₹5,400 | 8% | Stable |

You can update this monthly or quarterly to see your performance.

Option 2: Automated Tracking (Apps & Tools)

If you prefer automation, apps like:

- INDmoney

- ET Money

- Groww

- MoneyControl Portfolio Tracker

…can automatically fetch your mutual funds, stocks, and crypto data — and show total growth, asset allocation, and even tax reports.

Example:

Aman used INDmoney, and within 6 months, he realized 60% of his portfolio was in one sector — IT.

By rebalancing to include banking and pharma funds, he reduced risk and improved long-term returns.

How to Review Performance

Once you track, the next step is reviewing your portfolio — just like an annual health check-up.

What to Review:

- Goal alignment:

Are your investments still helping you achieve your original goals (house, retirement, education)? - Returns vs. Benchmark:

Compare your fund’s return with its benchmark or peers.

Example: If your large-cap fund gives 9% but the Nifty 100 gives 13%, your fund is underperforming. - Expense ratio:

High costs eat into returns. Prefer funds with lower expense ratios. - Risk exposure:

Is your portfolio too heavy on one sector or asset class? - Fund management changes:

A change in fund manager or strategy could affect performance.

The Annual Review That Saved ₹1 Lakh

Every January, Aman reviewed his portfolio. In one such review, he noticed one of his funds’ returns fell from 12% to 5% — while peers gave 11–13%.

He switched that SIP to a better-performing fund. Over the next 3 years, that small change helped him earn ₹1 lakh more.

That’s the power of simple, consistent reviews.

The Importance of Rebalancing

When you first start investing, you might decide a mix — say 70% equity, 30% debt.

But markets move.

A long bull run could push your equity portion to 85%, increasing risk without you noticing.

Or a market crash could drop it to 55%, slowing growth.

That’s where rebalancing comes in — bringing your portfolio back to your desired ratio.

Example:

Let’s say you invested ₹10 lakh — ₹7 lakh in stocks, ₹3 lakh in debt.

After a year:

- Stocks grow 20% → ₹8.4 lakh

- Debt grows 6% → ₹3.18 lakh

- Total = ₹11.58 lakh

Now, equity = 72.5% and debt = 27.5%.

You can rebalance by:

- Selling some equity and moving it to debt, or

- Investing new money in debt to restore the 70:30 ratio.

Key Idea:

Rebalancing helps you “buy low and sell high” naturally — without trying to time the market.

How to Continuously Improve as an Investor

The most successful investors share one secret:

They never stop learning.

Even Warren Buffett spends hours reading every day. Why? Because markets evolve — and your understanding should too.

Here’s how you can do it:

- Read regularly: Books like The Psychology of Money, Rich Dad Poor Dad, or blogs (like Target Prices ).

- Follow credible YouTube or podcasts: Learn from voices who simplify finance, not sensationalize it.

- Join communities: LinkedIn groups, Reddit investing forums, or your own “Target Prices” community can offer insights.

- Reflect on mistakes:

Everyone makes them — what matters is learning faster than others.

Riya, from our earlier story, learned after her first 5 years.

She started reading and reviewing — and within 2 more years, she outperformed Aman!

It’s never too late to start improving.

Key Takeaway

“Tracking is like getting regular health checkups for your money — it tells you what’s working, what’s weak, and what needs attention.”

Investing success doesn’t depend on how much you know at the start — it depends on how much you adapt and improve over time.

So if you’ve read this far — pat yourself on the back

You’re no longer a beginner; you’re on your way to becoming a confident, self-aware investor.